As an experienced Florida public insurance adjuster our company has seen it all. Roof damage, Flood Damage, Wind Damage, Large trees that have fallen and destroyed entire homes and much more.

Up until now, Florida has escaped a major category 5 hurricane. “Bite my tongue” However, this doesn’t mean Florida won’t see a slow moving category 5 hurricane hit Fort Lauderdale, Palm Beach County, Martin County or travel to the Gulf and pummel Tampa with 160 mile winds and flooding. If you live in Florida, then you should know that NOW is the time to prepare for the potential worst-case hurricane scenario.

As we move deeper into hurricane season, it’s becoming clearer that at some point a major category 4 or 5 hurricane will hit South Florida or the Gulf Coast creating extreme damage in communities such as Tampa, Fort Myers, Naples, Sarasota, or Fort Lauderdale, Palm Beach County, Martin County or Broward County.

The big question is; what would be the effect of a monster hurricane hitting your area? Extremely high winds, Storm Surge, Flooding, Power outages, Lightning strikes, Tornadoes, are all factors that South Florida and Gulf Coast homeowners need to consider. Currently we are seeing the effects from hurricane Ida as Ida, traveled up the Gulf coast hitting Louisiana and once again flooding New Orleans. Ida was so powerful it actually reversed the flow of the Mississippi River! Watching hurricane Ida it became apparent, the possibility of major damage could be in South Florida and the Gulf Coasts future. However, hurricane Ida didn’t stop once it hit landfall. The heavy rain caused major flooding in Philadelphia, New Jersey and New York City. This is the first time New York City has had this type of flood damage. As we move forward into the future, it’s clear that we have entered into a new era of hurricane and storm damage.

How would a worst-case scenario affect home damage insurance policies? From a Florida public insurance adjuster.

In addition to the physical damage, a major hurricane is going to wreak havoc with insurance companies. Check out this article on Florida’s shortage of insurance adjusters. Florida’s insurance adjuster shortage.

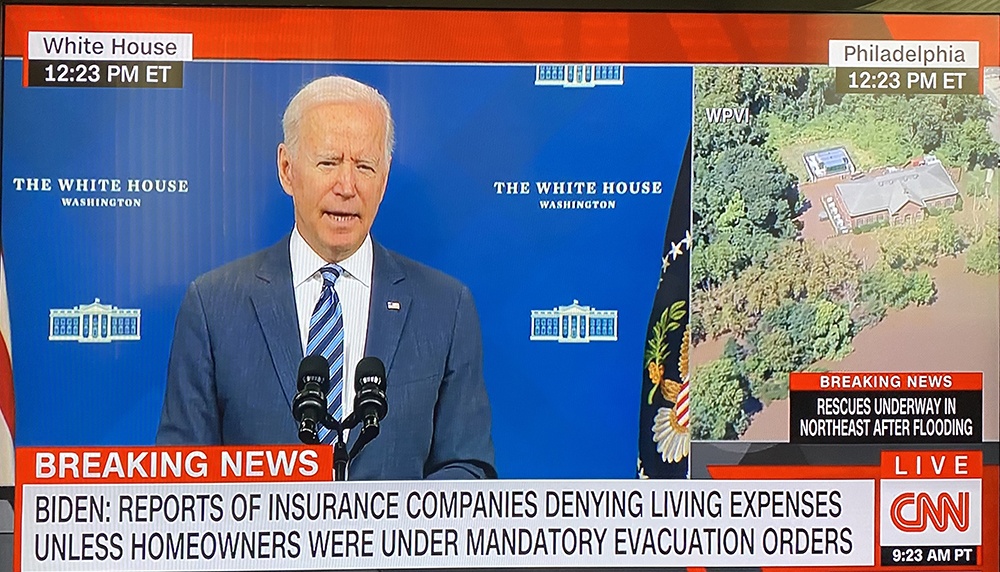

As a Florida public insurance adjuster who serves Palm Beach, Broward, and Martin counties, as well as the Gulf Coast and Tampa area, it’s become clear that hurricane Ida is another wake up call. The news stories that arose from Hurricane Ida were not just about the hurricane and storm damage that occurred. The news stories also involved how insurance companies avoided paying for some of the damage and relocation expenses. For example, there is now an issue in which some insurance companies refuse to pay homeowners evacuation costs, even though the policy included evacuation costs. This situation caused President Joe Biden to step in and ask insurance companies cover these costs. In other cases homeowners had been denied coverage, because at the time there was no mandatory evacuation order. There are also cases in which insurance companies are denying claims because some homeowners didn’t safeguard their homes according to the fine print in their policy. If you ask me, evacuating my home to save my life trumps the fine print hidden in my insurance policy.

If your home has sustained serious damage and your insurance company isn’t helping, then you may want to consider reaching out to a public insurance adjuster. Why would we suggest this course of action? The answer is related to the reason why we became a Florida public insurance adjuster in the first place. Before we started Fox public adjusters we were home contractors and home insurance agents. What we found were many dissatisfied homeowners who suffered home damage and couldn’t get help from their insurance company. Feeling really sorry for some of these homeowners, we felt our hands were tied by the insurance companies need to make high profits. We watched as homeowners faced long delays, denials and underpaid settlements. Finally we realized company insurance adjusters, we were not the solution, but part of the problem. Now, don’t get me wrong, home insurance companies provide a valuable and needed service. The concept that many homeowners pay a small amount on an annual basis for the sake of those facing complete or partial devastation is a godsend, especially for those South Florida homeowners who are in serious trouble. However, sometimes this model of homeowner protection is flawed.

How the home damage insurance company method is flawed?

When one company controls an entire industry, problems are bound to arise. The fact that a single company collects the money, then decides on the payout amount, means that the client, or in this case the homeowner, is at the mercy of the insurance company. For a homeowner hearing that you claim is denied, or receiving a letter that states your settlement will be much lower than the cost for repairs is nerve wracking. However, the situation doesn’t need to end with a denial letter.

There is another option. Homeowners can and should consider hiring a Florida public insurance adjuster, A public adjuster’s job is to represent the homeowner in a damage claim situation. Further more, receiving a portion of the insurance company’s settlement compensates a public adjuster. This shifts the incentive from, support the insurance company, to support the homeowner.

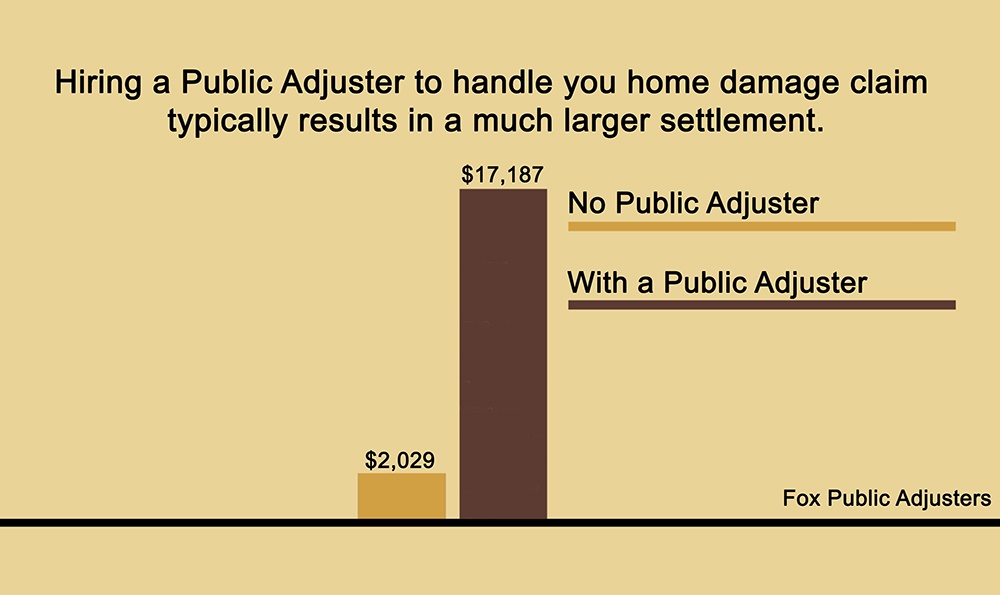

In addition, a public adjusters job is to know everything possible about how company insurance adjusters work, including how company insurance adjusters save company money. Now it may seem that the homeowner could loose money, because part of the settlement goes to the public adjuster, However, if you look at the facts you will find that in most cases, the homeowner comes out way ahead. Check out the chart below to see how much most homeowners receive when hiring a public adjuster vs. going it alone.

What would a worst-case scenario look like when a major hurricane hits South Florida?

First let’s consider this. As insurance companies go, there is a limited amount of insurance company adjusters. Even without a hurricane, many insurance adjusters are over worked, and need to service as many clients as possible. It’s a known fact that in many situations, insurance companies bring in adjusters from other states, just to handle the caseload. Imagine a category 4 or 5 hurricane hitting South Florida? How long do you suppose it will take for your home to be inspected? Given the amount of damage we have seen in the past, history tells us what we should expect.

First, let’s consider wind damage.

In our experience the first form of home damage is the result of the high winds a hurricane causes. A category 3 hurricane generates winds that range from 110 mph to 129 mph. The winds generated by a category three hurricane can seriously damage some homes and will completely destroy nearly all mobile homes. In addition the wind damage that would ravage South Florida could cause additional damage resulting from flying objects. While a category 3 hurricane could cause a wide range of damage, categories 4 & 5 hurricanes are much worse. How much worse? Read more.

While a the thought of a category 3 hurricane hitting South Florida or the Gulf Coast is bad enough, a category 4 or 5 hurricane hitting South Florida should be terrifying. A hurricane of this strength could rip off a homes roof with ease. Whether or not your home will survive is really a question of luck, and construction. While some newer homes that have been built to more stringent codes may survive, chances are they will sustain some damage. Category 4 hurricanes will have wind speeds of 130 to 156 mph. Category 5 hurricanes will have a wind speeds above 157.

As if wind damage is not enough, in a worst-case scenario, storm surge is the next unexpected foe

At this time, chances are your neighborhood is not covered in several feet of dirty, contaminated water. During a hurricane, your South Florida neighborhood could become an extension of the Atlantic Ocean. However storm surge is much worse than simply ocean water sloshing through your home. For those living in South Florida, the thoughts of the Atlantic Ocean bring visions of nice warm salt water, with waves, comfortable temperatures, the beach and healthy relaxation. This isn’t the case when ocean water reaches your home. In a storm surge situation, the water that blankets your neighborhood could contain a wide range of contaminants that have been carried along as the salt water travels across the earth. Included in storm surge water scientist have found a collection of oil and gas, toxins from drainage pipes, human waste, cleaning chemicals, and much more. Use you imagination for this one. One goes about daily life, they don’t think about all the oils, waste and poisons that are littering the ground. However, during a storm surge, all this dangerous stuff gets picked up, diluted and mixed in with the ocean water. This is not the type of water you want to swim in. Even if your home survives the hurricane strength winds, spending time wading through water from a storm surge is not in your best interest. This is simply another reason why homeowners should evacuate when a hurricane of category 4 or above is tracking toward South Florida. When deciding if you should evacuate it’s always a good idea to look at your area’s flood zone.

Although storm surge is different than flooding, insurance companies include both in the same category, or do they?

In a hurricane situation, the storm generated results in a continuous down pour of heavy rain. In some cases up to 6 inches of rainfall in one hour. In a normal situation this rain gets absorbed into the ground, or flows into lakes, streams, or is re-directed by a community flood management system. However, at some point this amount of rainfall becomes too much for the ground or flood management system to handle. Once a location has become overrun with rainwater, flooding starts. Depending on the travel speed of the hurricane this water could accumulate into large floods.

If you look at the graphic of South Florida you can see how most of the population lives between two coastal zones. Once a slow moving category 4-5 hurricane hits South Florida, dumping up to 6 inches of rain per hour, much of the area will become flooded. Just how flooded would South Florida become? Let’s consider this, when hurricane Dorian hit the Bahamas, it lingered over the same area for several days. Imagine several days of up to 6 inches of water per hour. Now granted, in a hurricane, the amount of rainfall is never consistent, but in the case of hurricane Dorian, many parts of the Bahamas were annihilated.

According to the best estimates a category 5 hurricanes hitting South Florida would create a combination of flooding from rain combined with storm surge. The result would cover Fort Lauderdale in several feet of water. Since Palm Beach County is located at a higher elevation it would not sustain the same level of flood waters, however the costal parts of Palm Beach County would be covered with flood and storm surge water.

What would a worst-case scenario look like when a major hurricane hits Tampa and the Gulf Coast?

First consider the fact that Tampa Bay gets narrower and becomes more shallow as the waterway heads inland. This means that when storm surge pushes water from the Gulf or Mexico toward Tampa the water is forced into a tighter and tighter space. This will cause the water level in the bay to rise to record levels.

Eventually the water will spill over and flood the area. This actually happened in when the Tampa Bay Hurricane hit in October of 1921. Back then the Tampa area was not as populated as it is today. If this occurred today, the damage would be far greater. Scientist predict that a category 5 hurricane would cause the water level to rise by 20 to 25 feet. This would flood Tampa and parts of Pinellas County would become islands. Given the fact that Tampa is much more populated than it was in 1921 the damage would be dramatic.

How do insurance companies pay flood or storm surge claims?

Generally flood and water damage from storm surge is both covered under a homeowner’s policy. However, some homeowners have had their claims denied because the storm surge was either caused by wind, or the property sustained a combination of both flooding and wind damage. This is when the line between having your claim paid or denied could get blurred. For example, most flood damage policies will cover damage from storm surges, however a standard home insurance plan that covers wind damage, probably won’t cover flood damage. This means that if you live in a coastal area, or in a potential flood zone you should purchase additional flood insurance. Don’t just assume because you have a homeowners policy you are covered.

If you are confused, you are not alone. When it comes to home damage policies confusion is what sometime leads to denied claims, underpaid claims, and other problems. Sure you could rely on your insurance agent for advise, but when damage happens it’s the company insurance adjuster who will ultimately determine your settlement. This is why many homeowners reach out to a public adjuster first. By having your claim handled by a Florida public insurance adjuster, you can feel secure knowing that your damage adjuster is looking out for you, the homeowner, and not the insurance company’s bottom line.

The key takeaways when Florida is faced with a worst-case hurricane scenario.

Prepare early

South Florida and Gulf Coast homeowners should start to prepare for hurricane season in June. This means, have you roof inspected for loose tiles that could fly off and become high speed projectiles, cut tree branches that could fall and cause roof damage.

Don’t assume that your home policy will cover flood damage.

Have an emergency kit

An emergency kit should include the following: Batteries, Matches, Tools for home repairs, A three-day supply of drinking water, canned food & a manual can opener, First aid supplies, A flashlight. If you have lived in South Florida or the Gulf Coast for a while, you should already have an emergency kit. So make it a point to go through your emergency kit and refresh some items that may have gone bad. Replace batteries; get new drinking water and so on.

Have a working power generator.

In a worst-case scenario you should expect the power to be out for a while. Having a gas powered or built in home generator will provide you with electricity for the days in which there is no power.

Check you hurricane shutters for missing parts.

When a hurricane tracks toward your area, having all the needed parts to cover your windows is a critical. By the time a hurricane starts getting close, the chances of finding the required parts becomes difficult.

Move your cars into a garage.

If your car is sitting outside during a hurricane, than your car will most likely suffer broken windows, and dents from flying debris.

Have your evacuation plan ready.

Our advice is to secure your home, follow the above list, and then get out of town. Given the fact that your home is most likely your largest investment, many people could understand your need to stay and hold down the fort, “so to speak”. However, it’s more important to look after your health, and let the insurance company cover any loss that may occur.

Finally,

Watch any hurricane news report and you will see stories of those homeowners who refuse to evacuate. Many Floridians romanticize the thought of being boarded up inside their home while hurricane force winds ravage Florida. For some, the thoughts of hurricane parties, catching up on reading, playing board games seems like a vacation. While these people are drawn to the adventure of hurricane excitement & possible injury, others watch the news and ask, why, is it worth it? Ultimately only you can decide to stay in your home or evacuate.